No matter how well you plan for and save for your retirement, you may find yourself reliant on Social Security benefits at some point during your senior years, regardless of how well you plan for and save for it. And it is for this reason that it is critical to file for benefits at the appropriate age.

In order to determine your monthly payment during retirement, your wage history — especially, the amount of money you were paid during your 35 most profitable years on the work — must be considered. However, whether or not you receive the entire benefit depends on when you sign up for it.

When you reach full retirement age, often known as FRA, you are entitled to receive your entire monthly pension. However, many people are unaware of their FRA and as a result, they file for Social Security benefits before they are eligible.

This could result in a significant reduction in your benefits, so it’s critical that you understand your FRA before enrolling.

The age at which you file for benefits has an impact on your benefits.

The earliest age at which you can file for Social Security benefits is 62. Meanwhile, there is no such thing as the “latest age to file for benefits,” because you are not obligated to do so at any point in your lifetime.

However, from a financial standpoint, there is no reason to postpone your filing until you reach the age of 70.

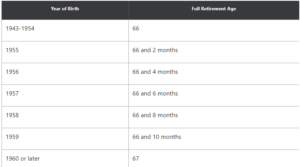

The full retirement age is right in the middle of that range, and you can use this table to figure out what it looks like for you:

Benefits are lowered by a particular amount for each month you claim benefits before the end of the fiscal year.

As a result, the earlier you join up, the greater the financial impact they incur. An FRA of 67, for example, will result in a 30 percent reduction in Social Security benefits if you file for benefits at age 62 with an FRA of 67 — and this reduction is usually permanent.

Although it is technically possible to undo your filing and be given a second chance to claim benefits, this is not the case in practice. Considering that doing so requires you to act swiftly and repay all of the benefits you have accrued, it is not an option for everyone.)

Meanwhile, for each month that you postpone filing for Social Security benefits past the Federal Reserve’s filing deadline, your benefits increase.

Recommended Read: Middle-Class Americans Will Receive More Stimulus Money During Tax Season: See If You Qualify?

Your benefits will increase by 24 percent if your FRA is 67, and you wait until you reach the age of 70, at which point delayed retirement credits cease to accrue. This benefit increase will be permanent.

You may now determine that filing for Social Security benefits before the Federal Reserve Act is the best option for you. Alternatively, you may elect to increase your benefits in order to make up for a 401(k) or IRA amount that you aren’t very pleased with.

What’s important to remember is that you can’t make an informed filing decision unless you know what your FRA looks like.

When should you apply for Social Security benefits?

The age at which you are eligible to claim benefits may be determined by a variety of circumstances, including:

- Your health as you approach retirement (if you don’t anticipate living a long life, filing for retirement earlier may be a good idea).

- The amount of money you have set aside for retirement.

- Your projected retirement expenses as well as your retirement objectives

To be clear, submitting a complaint with the FRA is not always the best option. However, it is critical that you are aware of this figure before making any decisions regarding your Social Security benefits.

And it is for this reason that it is so crucial to have this table on hand. Not only might you require it, but if you’re married, your spouse may also require it as you determine how to navigate the filing procedure together, so have it handy.

Most seniors are fully unaware of the $17,166 Social Security bonus they are entitled to.

When it comes to retirement savings, if you’re like the majority of Americans, you’re a few years (or more) behind.

However, a few little-known “Social Security secrets” may be able to assist you in ensuring a raise in your retirement income. For example, one simple approach could net you an extra $17,166 per year if you do it consistently enough.

We believe that if you understand how to optimize your Social Security benefits, you will be able to retire securely and with the peace of mind that we all desire.